Getting ready for an FHA appraisal? Knowing what to expect after having your offer on a home accepted will make the process smoother. This FHA appraisal checklist walks you through everything appraisers look for, common red flags to avoid, and how to prepare your home for success. Understanding FHA appraisal requirements can help you navigate one of the most important steps in the mortgage process.

An FHA appraisal is a required evaluation for anyone seeking an FHA loan that determines both the home’s market value and whether it meets government safety standards. This assessment protects both the borrower and the Federal Housing Administration by ensuring the property serves as adequate collateral.

Unlike conventional appraisals that focus mainly on market value, FHA appraisals examine the property’s condition, safety features, and structural integrity according to HUD’s minimum property standards. Only HUD-approved appraisers can perform these evaluations, and they must follow specific FHA appraisal guidelines during their inspection.

These same standards apply whether you’re purchasing a home or refinancing your existing loan, though some loan programs, like an FHA streamline refinance, may not require you to have another professional appraisal.

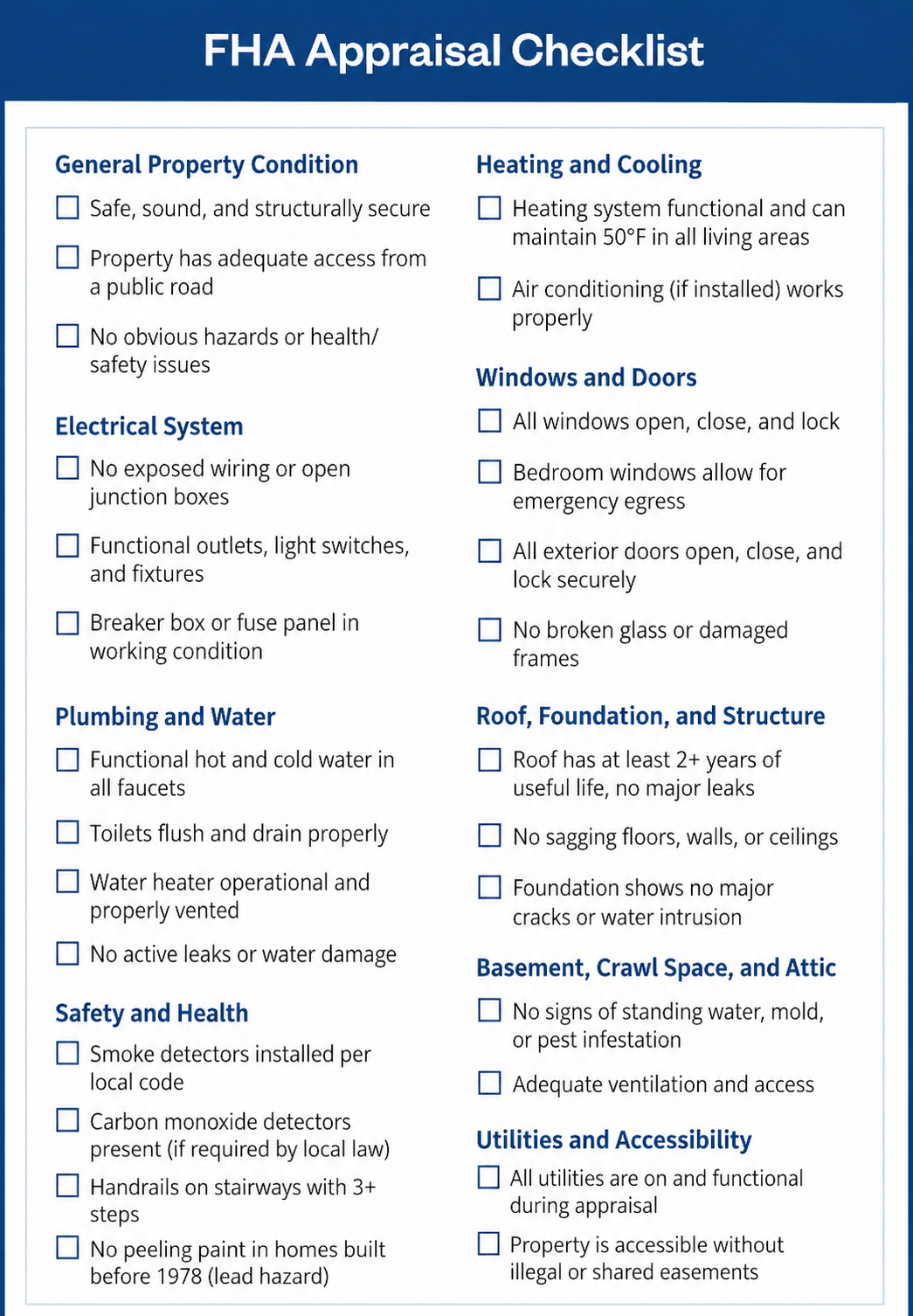

HUD’s minimum property standards are the foundation of every FHA home appraisal. These requirements focus on three core principles: The home must be safe for occupants, secure from intrusion, and structurally sound.

Safety is a major priority in FHA appraisal standards. Appraisers check for hazards, including lead-based paint, exposed electrical wiring, and missing safety features like handrails. The property must also have proper ventilation and adequate lighting in all living areas to ensure habitability.

Security requirements ensure proper locks and functioning windows, while structural soundness protects the FHA’s investment through stable foundations and roofs with at least two years of remaining life. The electrical system needs proper grounding and adequate capacity, while plumbing must provide hot and cold water with proper drainage.

When issues are identified, they typically must be corrected before loan approval.

Understanding FHA appraisal guidelines helps both buyers and sellers prepare for what appraisers will examine during their visit. Let’s take a look at what these are:

Here’s a comprehensive checklist covering the main items FHA appraisers examine during their inspection:

Several common issues can delay or derail FHA loan approval. Recognizing these red flags early can help buyers and sellers address problems before they become deal-breakers.

Most red flags require correction before closing. The appraiser must re-inspect after repairs, adding time to the process. Sellers often benefit from completing obvious repairs before listing, while buyers should consider professional inspections early in the process to avoid surprises.

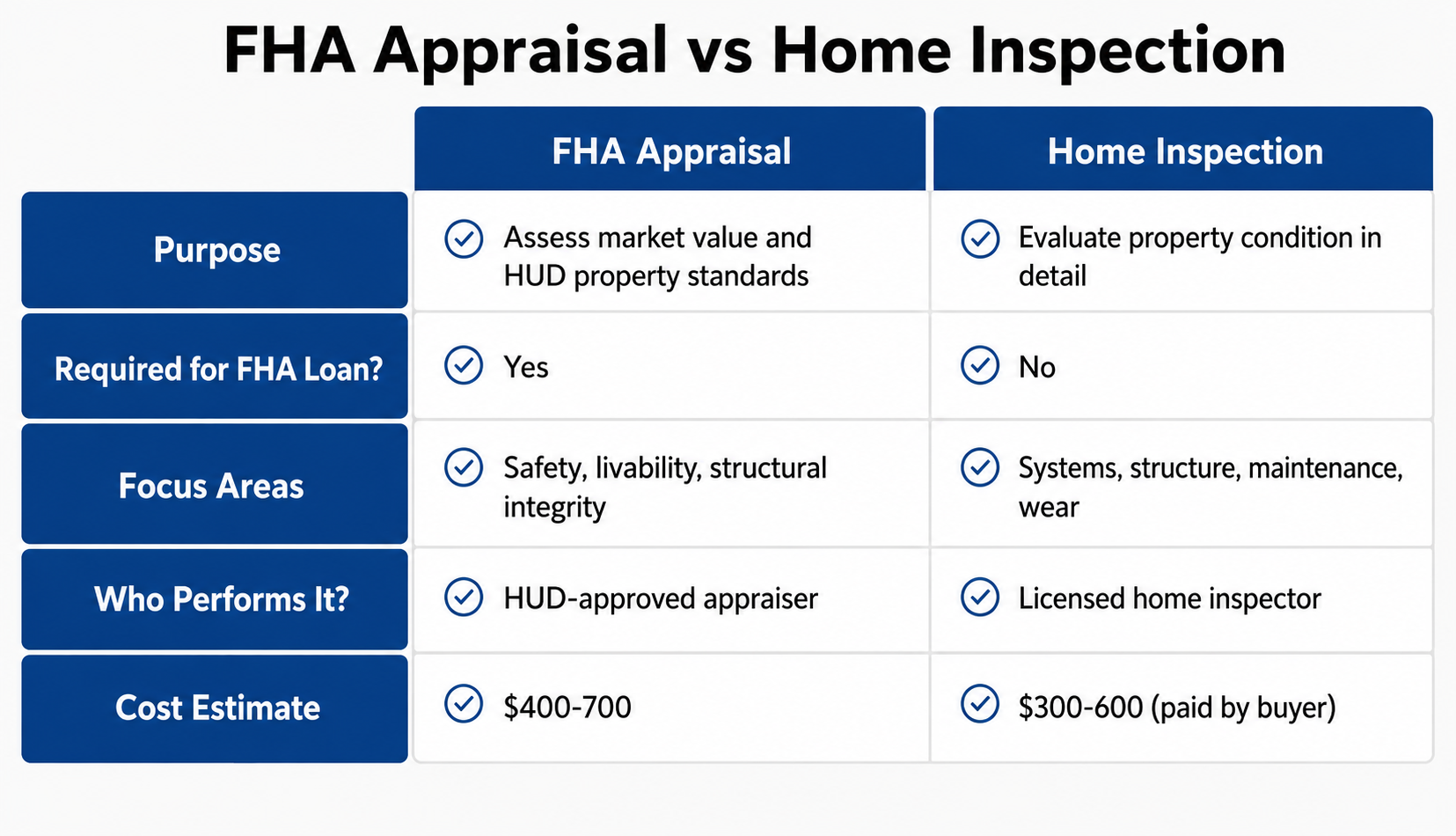

Many people confuse FHA appraisals with home inspections, but these serve different purposes in the home buying process. An FHA appraisal focuses specifically on safety and structural soundness as defined by HUD’s standards, checking for issues that could affect the government’s investment or pose immediate safety risks.

Home inspections provide more comprehensive evaluations, examining systems in greater detail and identifying potential problems that might not violate FHA standards but could cost homeowners money later. Professional home inspectors look at appliance conditions, minor electrical issues, plumbing efficiency, and cosmetic problems that don’t affect basic safety.

The timing and requirements also differ significantly. FHA appraisals are mandatory for all government-backed loans and must be completed by HUD-approved appraisers. Home inspections are optional but highly recommended, especially for first-time buyers who need to understand their investment fully.

For existing homeowners considering an FHA cash-out refinance, both evaluations help ensure the property maintains its value and condition. Smart buyers often schedule both evaluations to get the most complete picture of the property’s condition.

When FHA appraisals reveal issues that don’t meet HUD’s standards, several outcomes are possible depending on the severity of the problems and the willingness of parties to address them.

Required repairs are the most common result. The appraiser notes specific problems that must be corrected by licensed professionals, and the property must be re-inspected before loan approval. This process can add several weeks to the closing timeline and requires coordination between all parties. For buyers interested in properties needing significant work, FHA 203(k) loans allow financing both the purchase and renovation costs in one loan.

Parties can negotiate who pays for necessary repairs. Sellers might complete the work, provide buyer credits, or reduce the purchase price to make up for needed improvements. Buyers might choose to pay for repairs themselves if they’re getting a good deal or if the seller won’t address issues. Sometimes problems are too extensive or expensive, leading buyers to walk away entirely using appraisal contingencies in their contracts.

Each repair cycle and re-inspection adds time to the process, potentially requiring rate-lock extensions or alternative financing. Working with experienced lenders who understand different loan types can help minimize delays and ensure smooth communication throughout the process.